Bill Jackson, MERU Strategic Partner

Evaluating the Domestic Freight Market

Kathryn Dewing of MERU recently sat down with Bill Jackson, one of MERU’s Freight and Logistics Strategic Partners. As well as founding a 3PL and logistics company, Bill has partnered with major public and private equity owned companies for over two decades to help them solve their domestic logistics issues. He shared his thoughts on the current tumultuous situation in the domestic freight market.

This conversation has been edited for clarity and length.

MERU: Bill, thank you for taking the time today. Price increases and delays appear to be rampant in the domestic freight market at present. Can you embellish a bit more on what is going on?

Bill: Sure. Truckload spot rates are up 100% from June 2020 to June 2021. This increase in the spot rate is also putting upward pressure on contract rates, which are seeing double digit increases. Less-than-truckload (LTL) general rate increases (GRIs) are also up in the high single digits. On top of this there are capacity limitations, meaning that even if you pay the higher rates, you aren’t guaranteed good service levels.

On a positive note, in July, truckload rates were down 6% month over month from the previous month and there is a school of thought right now saying truckload rates have topped out.

MERU: Has the increased international freight costs impacted domestic rates?

Bill: The disruption and dislocation that has been caused by international freight markets has had an impact on domestic freight costs. You have containers that are out of position and a shortage of chassis and drivers all serving to increase costs. However, the overall American domestic market is over $100 billion and so whilst there is an impact there are plenty of other causes outside of international that are probably more significant.

MERU: What are the other causes that you mention?

Bill: There are a few factors.

- Supply and demand. Overall demand in the economy is increasing whereas the supply of trucks, terminals and workers are not expanding at the same pace

- Changing demand. Not only is there a demand/supply disequilibrium, the kind of demand is also changing. People want goods delivered to their homes even more now than before, but the system of trucks, drivers and terminals needed to efficiently accommodate this is still not in place

- Inventories at multi-year lows. Inventory to sales ratios are lower than they've been at any point since 1998 and potentially even earlier. Businesses need to replenish their safety stock, further driving demand

- Fuel costs. Diesel gasoline prices are up 37% year over year, so obviously that's going to increase freight prices

- Wage inflation for drivers. The combination of government regulations that reduce driver hours, the general aging of the US driver population (whose average age is now ~50 years) and the closure of new driver schools during the pandemic has resulted in a supply shortage of drivers, resulting in increased compensation to attract new drivers and retain existing ones

MERU: Do you think that these effects are long-term?

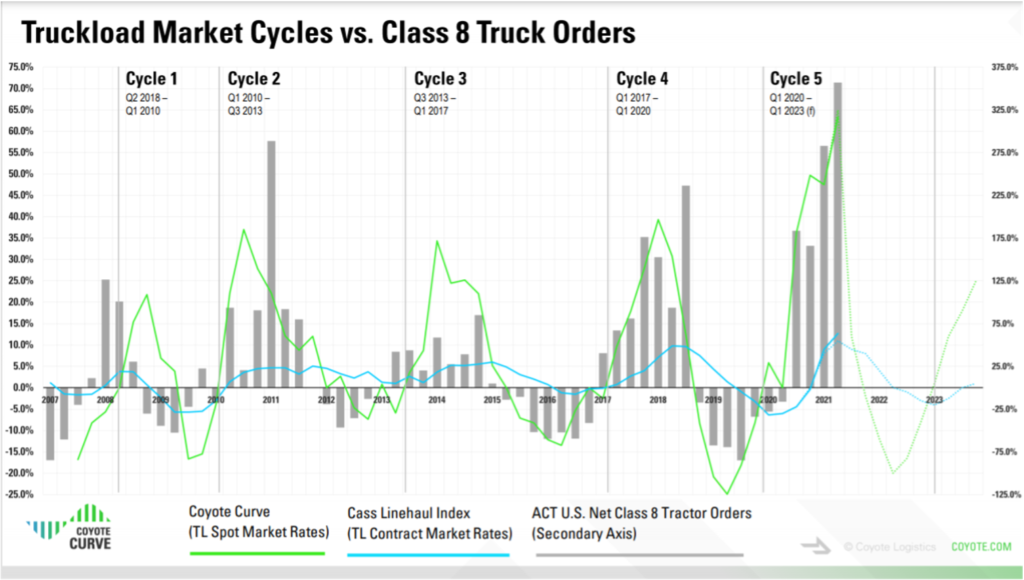

Bill: The trucking market is cyclical and as sure as I'm sitting here now, at some point over the next 4 years, we'll be talking about how rates have hit rock bottom. Right now, some economists say that we are at or near the top of the market, unless we have a major weather, financial or other event. Class 8 truck orders are increasing and more Motor Carrier (MC) numbers and DOT numbers are being approved so it is clear that new entrants are coming into the market, which will eventually force prices down. Today’s high rates allow a whole lot of inefficient trucking companies to stay in business. As rates fall, those carriers go out of business, putting a floor on rates and allowing the cycle to start anew.

In the longer term, the next 10-20 years, if wages stay high, then autonomous trucking is likely to become a bigger part of the market, reducing the need for drivers. That is the potential long-term impact.

MERU: What impact have these increased costs had on your clients?

Bill: Everybody is feeling some level of pain. Costs are up for everyone, service quality is down and there’s uncertainty around lead times. The question that I focus on with clients is “Is this pain short term or long term?” Long-term pain means that your logistics function fails to provide consistent service to your customer and your customer leaves you - losing your customer is permanent pain. Paying more for trucking is short term (plus you may be able to pass along some part of the higher cost) – but rates will flip at some point. So you have to decide whether you want to keep that customer at shorter term higher rates or potentially lose the customer by trying to use the cheapest carriers you can find. Even clients that own their fleets are not immune as they still face increased input pricing e.g., spare parts, maintenance, repairs, fuel, and driver costs as well as insurance.

MERU: What have your clients done to counteract this?

Bill: Thoughtful clients have used this as an opportunity to reevaluate how they manage logistics. In most manufacturing and distribution companies, logistics costs are usually one of the top two or three spend categories but usually logistics is only focused on when something's broken. You'll have logistics departments that have practices like sending out blast emails to hundreds of carriers or brokers, or they'll invest in websites that effectively do the same thing. This is not the optimal way of doing logistics.

What needs to happen is you need to have data driving your decisions. There are many sophisticated freight vendors out there who can provide strong analytics if your company lacks the resources to do it yourself. If you're going to use a broker, you need to benchmark that broker’s performance as well as having a transparent relationship with your broker regarding mark ups and pricing.

MERU: Have your clients been able to lock into contracts to counteract volatile spot pricing?

Bill: Everybody has tried, with mixed results. On the truckload side, there's been an increase in tender rejections. That means that carriers under contract are rejecting orders that are tendered to them that they should be picking up. They are rejecting them as carriers will make a lot more money on the spot market. Shippers don’t have a lot of options right now other than to track which carriers are honoring agreements and which are chasing the money.

In the LTL space, some clients have had more luck than others. Ironically, we have a couple clients where we reduced their LTL rates by double digits during 2Q21 – so opportunity is out there for data-focused clients. Additionally, LTL carriers are not fined for missing pickups so what's happening is they don't have to reject the contract – they simply don’t show up until it profits them. LTL carriers are also embargoing certain regions of the country because they are losing money going there.

MERU: What is the best way to prevent contract rejection by a carrier?

Bill: The carrier holds a certain level of power right now. The level of power depends on the sophistication of the shipper. Shippers that maintain carrier scorecards, make it easy on drivers to pickup and deliver, and have rigorous tracking of data are able to get better performance and a lower tender rejection than shippers that don't do that.

MERU: For those that need to go to the spot market, what advice would you give them to mitigate the costs?

Bill: There's not really a one size fits all answer but I do have a couple of thoughts.

- Have data drive your decisions. Measure whether the mitigation strategies that you are putting in place are actually helping. Set a baseline for your costs and service levels and measure how the changes that you are making are impacting costs. A lot of people are just fighting fires right now and not taking a look to see if there is a better way to do it

- Be a better customer. Ask yourself, are you making yourself an easier customer for your logistics partners? Can you make simple, relatively cost neutral changes that are attractive to carriers? For example, can you close your yard later in the day to enable later shipments to come in? There is a focus on labor costs and reducing overtime but if you're trying to keep a customer, you need to come up with strategies to keep your shipments on schedule

- Pay and retention. Labor shortages are out there and so loading trucks quickly is often tough for shippers. But I can tell you, if a truck comes in and you keep a driver longer than your contractual amount of time, which is usually two hours, and then you don't pay that driver for his lost time, he is not coming back

- Parking. This is a huge area that makes a difference. If the driver has to wait overnight and the closest parking spaces to your facility are 30 miles away, he'll find another load and you're not going to be able to get your load covered

- Billing. Are your carriers billing you accurately? Especially in the LTL space, ~30% or more of invoices received from carriers are inaccurate in some material way, and in most cases the variance favors the carrier. Check those invoices, make sure the documentation is correct and the billing charges match up with what you are contractually bound to do

- Management mindset. We are at the top of the market right now so once you see freight costs fall, that doesn't mean that your logistics problems are fixed. As rates come down, it doesn't mean that your logistics department is suddenly amazing. In order to not repeat the cycle ask yourself, how am I performing against the market benchmark?

MERU: Has the freight cost made companies reconsider where to locate their warehousing?

Bill: A vast majority of our client work at present is network optimization. Clients are evaluating all options including warehouse locations. Even if lease agreements are far out in the future, you can still plan today for where you want to be. In many cases where you have a warehouse now was a decision that was made a decade ago and many factors - shifting population, shifting demand, the need to locate warehouses closer to consumers – have changed significantly in the last decade. For those where it makes sense, the identified savings have been enormous, generally speaking.

MERU: Have there been any instances where it makes sense to break current leases?

Bill: For some clients from an economics perspective, it makes sense to break the lease. However, other factors such as inventory issues and working capital being tied up as well as a lot of customer bases nervous already, it may not be the optimal timing.

MERU: What are the lasting effects that you see taking place due to this freight cost environment?

Bill: A lasting effect will be the acceleration of acceptance of managed transportation solutions. Instead of sending blast emails to hundreds of different carriers, there will be a move to more defined processes. That is happening already. An example of this is UBER Freight’s acquisition of Transplace in July for ~$2.25bn[1]. It is a huge area for growth.

In the long run, if wages remain elevated it might serve to accelerate autonomous trucking adoption. When you start having autonomous trucking, combined with logistics optimization, you are going to start seeing a long term reduction in overall supply chain costs

MERU: What is going to bring the prices down or at least stop them increasing?

Bill: I'm back to supply and demand. Supply of trucks and drivers needs to increase and/or demand needs to increase at a slower rate than supply. Class 8 orders and new carriers are being approved by the government at record rates. Driver schools are back in business and there aren't any government regulations on the near-term horizon - that's all good news on the supply side in terms of rates coming down.

On the demand side, inventories returning to normal and returning to a sustainable GDP growth rate are both going to help. Obviously, if we go into recession, that will have an impact but my hope is that there is a return to standard GDP growth rather than a recession.

MERU: What indicators are you looking at to gauge when you think this will be the case?

Bill: Inventory to sales ratio, PMI (Purchasing Managers Index), Class 8 orders / approval of new MC numbers by the government. Those are big ones that are usually predictors of a move in the cycle.

MERU: What impact do you think the Delta variant will have on prices?

Bill: If the Delta variant causes a return to mask mandates and social distancing it makes it harder to load and unload trucks. This slows down the supply chain. Drivers only have a certain amount of time that they’re allowed to be driving or on duty and if it took an hour to load a truck and now it takes two hours, that's one hour less drive time. This adds up to less shipments per driver than previously and will slow down the entire supply chain. As such, domestic transportation costs will go up because you need more trucks to cover loads and there are only so many trucks.

MERU: Thank you for taking the time today, Bill.

[1] Uber Freight to Acquire Transplace in $2.2bn Deal (supplychaindigital.com)