David Lloyd, MERU Strategic Partner

Navigating Headwinds in the Restaurant Industry with David Lloyd

Hershel Perlmutter and Kyle Sturgeon of MERU recently sat down with David Lloyd, one of MERU's Food & Restaurant Strategic Partners. David first became involved in the restaurant and food space when he stepped in as CFO for Taco Cabana, one of his clients at Deloitte. Since then, David has been involved with several other restaurant chains as CFO, President, and CEO. More recently, he has served on several boards and in advisory roles for popular restaurant chains across the country, including Cosi, Uno Pizzeria & Grill, Boqueria Restaurants, and Punch Bowl Social.

This conversation has been edited for clarity and length.

MERU: Can you tell us your background and how you became interested in the restaurant space?

David: I started working for Deloitte, mostly on the audit side with a little bit of consulting and IT stuff back in the day. Then some of my clients became more restaurant retail oriented, and I actually went to work as CFO for one of my clients that was a restaurant company called Taco Cabana. That was back in 1994, and we eventually sold that at the end of 2000 to Carrols Restaurant Group, which is the largest Burger King franchisee.

Then through connections, I was introduced to people in the process of looking at Taco Bueno. We partnered with a PE firm out of New York and bought them in 2001, sold it four years later, and it was a great deal. The PE firm also owned a company in Boston called Bertucci’s, so for about a year we were running both concepts (Taco Bueno and Bertucci’s). I was with Bertucci’s for a total of 9 years.

Since 2013, I’ve gotten involved with various concepts at different stages. Currently sitting on the board for three different concepts in the restaurant space.

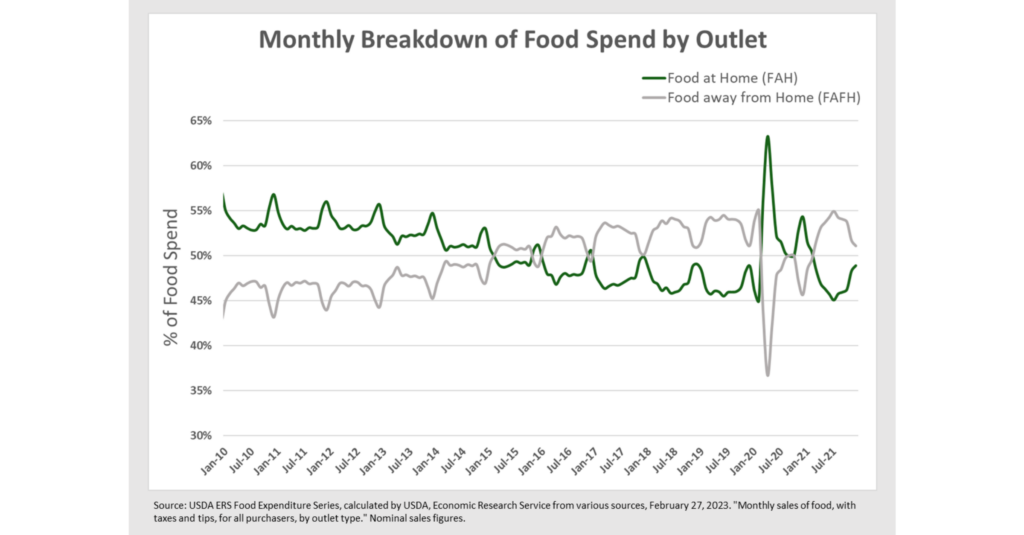

MERU: We’d love to shift to talk about some trends we’re seeing in the restaurant space today. Starting with on-premise versus off-premise dining. Over the last decade, we’ve seen consumers’ % of spend on food away from home (FAFH) steadily increase and even overtake consumers’ % of spend on food at home (FAH). Where do you think this trend will be heading in the years to come, and how will Covid have impacted the direction?

David: Yep. I don't think there will be a reversion all the way to pre-Covid figures. People have gotten used to off-prem, the consumer will continue to demand it, and there will be a supply. That being said, I don't think it's going to stay as elevated as it was the last couple of years. I think there's always a need or a want on the part of consumers to get out and have an experience. For example, I sit on the board of Punch Bowl Social. There’s good food, but we also want people to come out and gather, enjoy, have parties. The whole idea of parties and social gatherings is a big deal. Similarly, last week Dave & Buster's announced their earnings, and they're seeing that come back. So yeah, I think [off-prem] is not going back to where it was, but it's not going to grow forever and every restaurant is not going to be a virtual restaurant (also known as a ghost kitchen; a restaurant that only serves customers via delivery and pick-up).

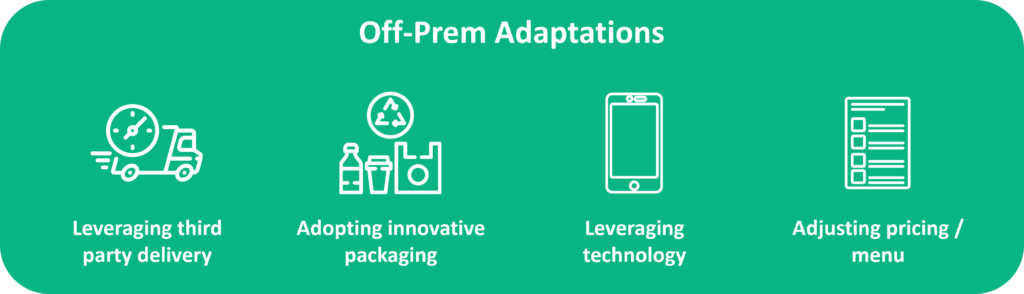

MERU: In what ways have you seen restaurants adapt to off-prem consumption in the past couple of years? And how have you seen it differ by the type of restaurant, like fast casual versus full-service?

David: Sure, the fast casual and quick service restaurants (QSRs) were loving life. That was exactly where they were best positioned, and they could take advantage of all the off-premise. The full-service guys really had to play catch up, which they did. I think a lot of them never thought they'd get into third party delivery or make it easier for guests to come pick-up, but they had to. Ways they’ve done that include:

- Leveraging third party deliver. That’s the biggest and most obvious one that will continue in some fashion, despite some pushback against it by the restaurants. As long as the consumer is willing to pay the premium for having food delivered to their house, it’s not going away.

- Adopting innovative packaging. Coming up with more innovative and better packaging. Figuring out the easiest, cheapest way to do it and still look presentable by the time it gets home.

- Leveraging technology. Obviously, all these apps where you can order literally anything from anywhere. Everyone’s so used to that, it’s not going anywhere.

- Adjusted pricing / menu. In the beginning, when third party delivery was getting started, you had to pay 30% to the delivery companies and have the same menu available that you did in the restaurant. That just doesn’t work for the restaurants. Now, restaurants are adding anywhere from 15% to 25% markup over their menu prices. Some are shrinking the menu because there’s some stuff that doesn’t travel well or present well to the consumers. And they’re pushing back hard on the 30% to the delivery companies and getting some relief, but it’s still going to be a premium to the customer.

MERU: Have you seen changes in the design of restaurant seating?

David: Yeah, in terms of seating, you’re starting to see everyone build smaller store prototypes with less seating available. It’ll be interesting to see if they can make it work because the economics are really tough. They’ll have to make up for a lot of that business with off-premise, certainly in the casual dining or the higher end space. Fast casual, on the other hand, has adapted quite well. The “older” fast casual brands from 10 years ago have already adapted by making carry-out very effective in most cases.

So, I think yeah, the trend is definitely going to be for less seating, certainly at the middle and lower end, fast casual, fast food, QSR. And the casual dining guys are trying that. It remains to be seen whether the numbers will work. This has happened before, but it’s hard to make the financials work because you can’t shrink your kitchen. And that’s where a ton of the money in construction is built up.

MERU: What about changes in the design of the kitchen itself?

David: I think the designs of the kitchen will adjust to the menu. We’re seeing menus shrinking, and as the menu shrinks and new restaurants are built, the kitchen is going to get simplified. It’s also really hard and expensive to get cooks. So the simpler you can make things in the back of the house, the more sustainable the model is going to be.

There’s always going to be high-end restaurants who are chef-driven and the kind of places that I'm sure all of us like to go to. But for the everyday kind of place, they're going to have to figure out how to change their physical plant as they go forward.

MERU: That makes sense, and then of course you have the front of the house technology. How are you seeing restaurants bringing in new point of sale (POS) systems or simplifying the ordering process?

David: That’s definitely happening, even in the older brands right now. Historically, a big barrier to that for the bigger, legacy chains had been their longstanding POS hardware contracts. They were clunky and old, and if you had 500 or 1,000 restaurants, it was a pain to change and really expensive. But these legacy chains are coming around now.

In terms of the technology, everything’s going to be in the cloud. It’s very cheap to deploy and much more user friendly for people who are comfortable with the tech. And I think today, everybody’s so used to ordering and paying with your phone or card electronically. That’s going to change the labor model for front of the house dramatically.

Because, say maybe you need 30 servers to run a restaurant. What you really want are 15 people who are really good, talking to the guests, and a bunch of people behind the scenes, bringing drinks and food out and clearing the table, and all that kind of stuff. It was kind of hard to do when the server also had to write something down and go punch it in. It was a process. That barrier, if it's not completely gone, it's certainly going away. That technology is going to change the whole interface with the guest.

MERU: And on the point of interfacing with guests, when you're adding extra capacity in the summer months in terms of outdoor dining, how sophisticated are the establishments in ensuring that the kitchen can keep up with the additional demand that might be occurring during those months?

David: I think existing restaurants were built to serve indoor seats. If their indoor seats are full and they've just added 20 or 30 seats outside, that's a problem. Some of the other things we were talking about might counteract that: the smaller menus, the easier to execute back of the house kind of techniques, that will help, but it will absolutely slow down the kitchen service.

I think new restaurants are going to get built with that in mind, and there's really going to be more of an emphasis on outdoor eating. In ways that, you can cover it and use it as three season seating in places where the weather is amenable.

MERU: Let’s shift to the customer. What are some best practices that you've seen restaurants do for owning their customers these days? How do they establish customer loyalty?

David: Yeah. That's the big question. The knee jerk reaction is loyalty programs, which are getting more sophisticated and more accepted. It’s a great way to connect with your guests. And when you talk about how you’re connecting with guests, it’s got to be one-on-one. The idea of doing mass advertising just doesn’t make any sense. Who watches TV and commercials anymore?

So, loyalty programs or apps just allow so many more ways to connect one-on-one with customers and have individual offers. Everyone loves the game of loyalty points.

MERU: Do you see any risk of there being loyalty fatigue amongst consumers, with all these restaurants starting to do it now?

David: No doubt. But some of it is self-selecting. When you get people to sign up for the loyalty program, they’re probably your most loyal customers. Especially when you’re first starting the program, so that’s the self-selecting part. But their spend per person every time they go in is 15% to 20% higher. So whatever you're giving them to come back that one more time is well worth it.

But in terms of consumer fatigue, of course. Because it's still limiting to go to one place all the time, no matter how much you love it. I mean, you get fatigued eating the same food. But I don't know how you can ever measure that.

MERU: Are there any other effective marketing strategies that you've seen restaurants adopt?

David: I think everyone’s trying to go all in on the web ads. The providers [Google, Facebook, etc.] are always trying to show you how valuable it is and how much money you’re making every time you spend to get a click. The only thing I’d say to that is what’s the first thing that got cut as budgets tightened up over the last six months? People cut digital ads because it’s really hard to pin down the actual payback there. For example, if you watch a lot of YouTube videos, you get a lot of commercials that may or may not be relevant to you.

An interesting one that people are trying is celebrity partnerships. One that comes to mind is Naomi Osaka and Sweetgreen. But Burger King has one, McDonald’s has one, and Chili’s has one too. And if you’re a fan of that celebrity, is that halo going to rub off on the brand? It’s definitely something different that people are trying.

MERU: I think that covers our three main topics and now just some closing questions to get your thoughts on the broader industry. As we think about the upcoming year, what steps do you think restaurants should take in preparing for a potential recession?

David: This will be the CFO talking in me, but conserve cash, slow growth, hunker down. The one thing I would say that they should be doing, but they tend not to, is that’s the time to really continue to invest in your restaurants. Because the first things to get cut are maintenance and remodels. Then later, when things have “normalized,” the restaurant looks awful. And consumers notice that right away. So, if times are tough and you walk into your favorite restaurant and it looks like it’s deteriorating, that makes a difference and indicates to the consumer that you’re not doing well. So continue to invest in your brand.

The other thing is to close restaurants aggressively – be aggressive about getting out of bad places, especially during a recession. Hire people to get you out of those things.

MERU: And in terms of KPIs or the metrics that you’d manage by, from both a financial and operational lens, what do you find to be the most helpful?

David: At the end of the day, if you’re running the company, the only one that matters is ROI, otherwise you can’t attract capital. In order to do that, you need to look at prime costs (food plus labor), which has to be less than 60% otherwise you don’t have a sustainable model. When I’m talking to private equity firms who are looking at restaurants, that’s the first metric they look at.

The other big one is to focus on labor. Looking at sales per labor hours as an efficiency metric. And that way you can separate back of the house from front of the house and know, how efficient am I? And that's something you can compare then across your portfolio as opposed to looking at it as a percentage, because labor costs are higher in San Francisco than it's going to be in Omaha.

MERU: And finally, what sort of disruption do you expect to see in the space in the coming years?

David: Labor will be a big one. The lack of skilled labor and how hard it is to be in the back of the house of a restaurant. People don’t want to do it, especially when they can make more money doing something less taxing. And so that brings on everything we've talked about from automation to menu simplification, to outsourcing the production to some extent. Those are going to accelerate.

The other big one will be legislation, and when are you going to hit that point where it just no longer makes sense to do business in Chicago or San Francisco, or New York, or whatever the case may be? So ultimately that becomes sort of a tax on the consumer because those higher costs just get passed through.

MERU: Thank you so much, David.

1. Monthly Breakdown of Food Spend by Outlet, Food Expenditure Series USDA ERS

Authored by: Hershel Perlmutter, Director, in collaboration with Kyle Sturgeon, Managing Partner, and Lucy Huang.